European Sustainability Reporting Standards

CSRD and ESRS establish a mandatory, standardized sustainability reporting framework in the EU, with revised and clarified standards designed to improve comparability, auditability, and decision-useful data.

The Corporate Sustainability Reporting Directive (CSRD) fundamentally reshapes non-financial reporting. It expands the scope of reporting companies, requires assurance, and mandates the use of the European Sustainability Reporting Standards (ESRS) as the single reporting language.

CSRD essentials

Applies to large EU companies, listed SMEs (with transitional relief), and non-EU companies with significant EU activity.

Requires double materiality assessment as a formal, auditable process.

Integrates sustainability information into management reporting and risk governance.

Phased application starting with FY2024 reporting (published in 2025).

Revisions focus on:

Clearer data point definitions and reduction of ambiguity.

Stronger linkage between policies, actions, targets, and metrics.

Improved alignment with EU legislation (Taxonomy, SFDR, due diligence laws).

Sector-specific ESRS have been postponed; reporting remains sector-agnostic for now.

Why this matters

CSRD shifts sustainability reporting from narrative disclosure to structured, comparable data.

ESRS requires systems, not spreadsheets.

Companies that treat ESRS as a data architecture challenge, not a reporting exercise, will reduce risk and gain strategic insight.

CSRD and ESRS are not about more reporting. They are about enforceable transparency at scale.

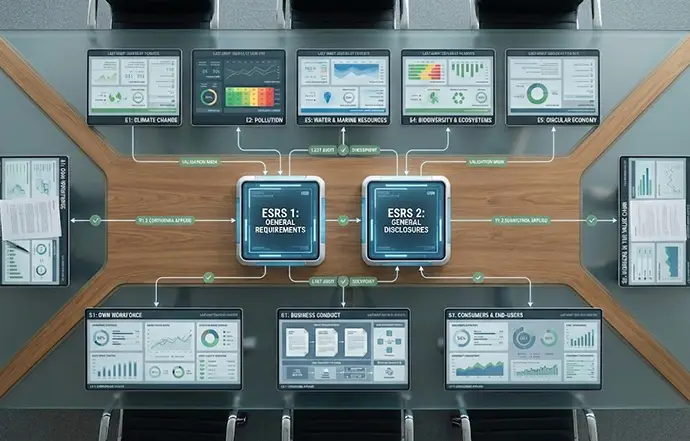

ESRS structure

Cross-cutting standards:

ESRS 1 (General Requirements)

ESRS 2 (General Disclosures)

Topical standards:

Environmental (E1–E5)

Social (S1–S4)

Governance (G1)

Revised and clarified standards

The ESRS Set 1 was adopted via Delegated Act in 2023 and subsequently clarified through official corrigenda and implementation guidance.

Sustainability readiness & Risk assessment

Assess your Sustainability Maturity Level & Address your Sustainability-related Risks.